The FCC’s Wireline Competition Bureau released the latest streamlined E-rate appeal and waiver decisions on June 1, 2026 (DA 26-497). This month’s order is smaller in volume than May’s release (read our full May article) but contains decisions along two themes that offer particularly clear guidance on where the Bureau draws the line between relief and denial.

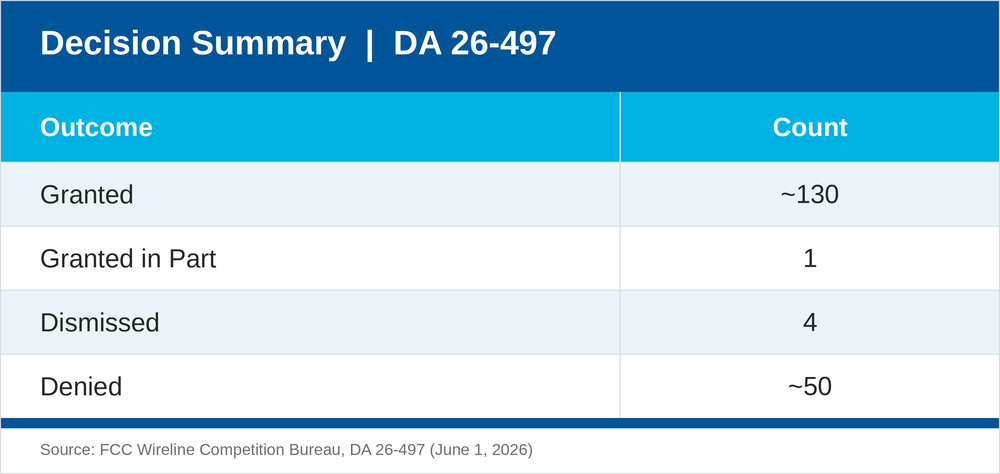

Late-filed FY2026 Form 471 applications again dominate the granted category. The denial category is proportionally larger than last month, with more than 30 applicants denied for late Form 471 filings and ten denied for late invoices or invoice deadline extension requests.

Key Themes and Takeaways

The Form 471 Window: What Separates Grants from Denials

This order continues the pattern from May. Applicants who filed within 14 days of the window closing generally received relief. Applicants who filed beyond 14 days without specific, documented special circumstances did not.

The Bureau granted relief in two situations that go beyond the standard 14-day window. Seven applicants received waiver approvals because an unexpected serious illness or death in the family of the staff member responsible for E-rate prevented timely filing. One applicant filed more than 30 days late due to serious illness and still received relief. The Bureau has long recognized genuine emergencies as special circumstances, but documentation is essential. A general claim of hardship is not sufficient.

The “Granted in Part” decision is also instructive. A group of approximately 50 applicants filed a single consolidated waiver request. The Bureau granted relief for nearly all of them but denied three because those applicants failed to individually demonstrate special circumstances. A group filing does not protect every member if the underlying facts are not adequately documented for each applicant. The Bureau also used this order to encourage parties with multiple applications based on the same facts to file one consolidated waiver with a list of application numbers attached, rather than separate submissions for each application.

Invoicing Deadlines: An Active Specialized Review Does Not Automatically Pause Deadlines

One reconsideration decision is the most significant in this order. It involves a conflict between a compliance review and an invoicing deadline, a situation many applicants could find themselves in.

The applicant was under an active USAC Special Compliance Information Request when its October 28, 2025 BEAR invoicing deadline arrived. USAC’s notice stated that “no new funding commitments or payments for existing funding commitments will be processed until this review is complete.” The applicant interpreted “payments” to include BEAR submissions and halted all invoicing activity. This was not a position developed after the fact. The applicant’s E-rate administrator documented the interpretation in real time, noting internally that “all reimbursements from all applications [were] on hold.” The notice language was genuinely ambiguous, and the applicant’s reading of it was not unreasonable.

The Bureau nonetheless upheld the denial. Regardless of how the applicant interpreted the communication, it could have requested the automatic 120-day invoice filing extension before the October 28 deadline and did not. That failure was the dispositive issue. The existence of an active audit or compliance review does not automatically pause invoicing deadlines, even when USAC communications create genuine uncertainty about whether payment activity should continue.

Any applicant or service provider currently under a USAC compliance review should treat invoicing deadlines as unchanged. If there is any uncertainty about whether invoicing should proceed, the correct response is to request the 120-day extension before the deadline as a protective measure. Doing so costs nothing and preserves every option. Seeking a waiver after the deadline has passed, even with a well-documented and reasonable rationale, is a significantly harder path.

Across both themes in this order, the applicants who received relief had documentation, clear timelines, and specific circumstances that explained what went wrong. The applicants who did not receive relief fell short on at least one of those elements. That standard is consistent and does not change based on how sympathetic the underlying situation may be.

Wondering how a situation like this gets handled? Our Guides work with applicants through active reviews and invoice deadlines every filing year. Learn what working with a Guide looks like.