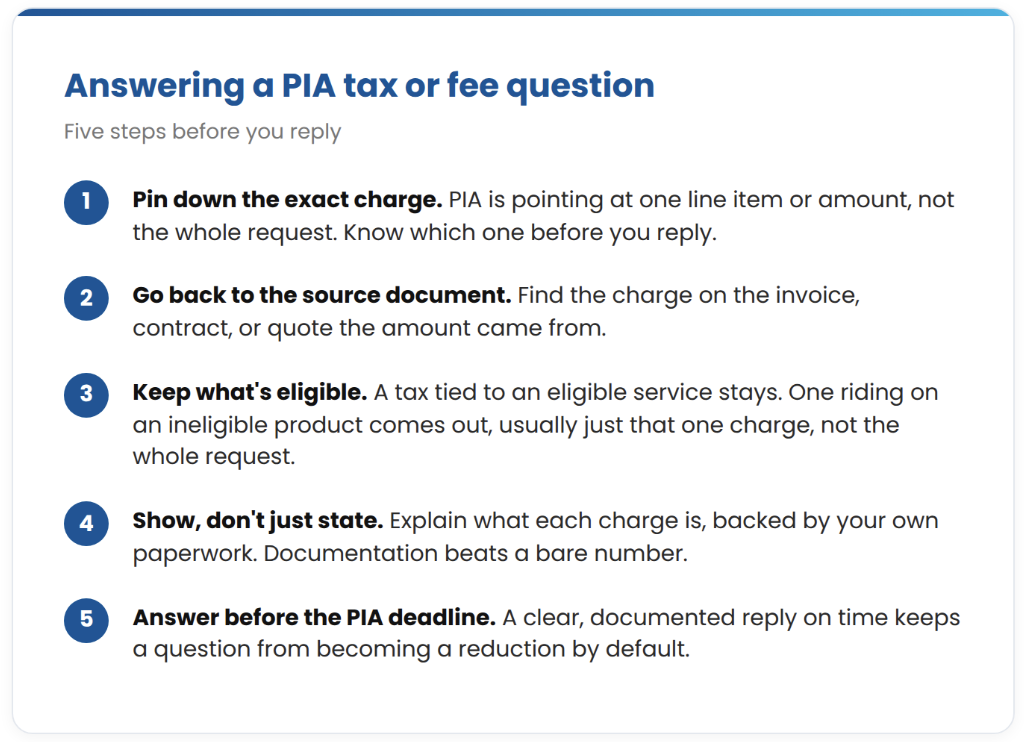

If you are working through Program Integrity Assurance (PIA) review and a question comes up about a tax, fee, or surcharge, start with this: these charges are often eligible. USAC asking about one does not mean it has to come off your request. It means the reviewer needs to understand what the charge is.

That distinction matters, because the instinct when a question lands is sometimes to pull every tax and fee out to be safe. That can cost you funding you were entitled to. Taxes, surcharges, and certain reasonable charges can be eligible when they are tied to an eligible product or service. The goal of your response is not to strip them; it is to show clearly which ones belong.

We looked at FY2025 decision data to see how these questions actually resolved, and the patterns are useful if you find yourself answering one now.

Why taxes and fees get questioned

The most common reason a tax or fee draws a question is bundling. Invoices and contracts often combine eligible service costs with taxes, surcharges, provider fees, and administrative charges in one total or one line item. When those amounts are lumped together, the reviewer can’t tell from the request alone what belongs and what doesn’t, so they ask. Your response just needs to separate it for them.

What the FY2025 data shows

Looking across the FY2025 decision data in E-rate Manager®, tax, fee, or surcharge language showed up in more than 1,400 funding requests. In the large majority of those, USAC trimmed the specific charge rather than denying the line item, so over nine in ten kept their funding for the eligible service. The line item rarely disappears, but the reduction is real money off the top. Taxes and fees are not the only place a small detail can move your funding. Enrollment changes did the same thing in FY2025, here is what the data showed.

Three ways this played out last year

A school had filed one Internet Access line item that combined fiber service with taxes and USF fees. The USAC reviewer split it into two line items to separate the fee portion from the eligible service, matching the applicant’s own documentation. Nothing was denied; the charges were just sorted out.

A district’s Internet Access request was reduced to remove a portion identified as universal service fund administrative fees. Customer charges for universal service fees are eligible, but charges for USF administration are not, and that distinction is easy to miss when it’s buried in a bill.

A school’s Internal Connections request was trimmed to remove an ineligible equipment item along with the sales tax riding on that specific item. The tax wasn’t the problem on its own. It followed the ineligible product.

In none of these cases was the applicant doing anything wrong on purpose. The charge was simply bundled or described in a way that made the eligible and ineligible portions hard to separate. The applicants who came through these with the least disruption were the ones who could show, clearly and quickly, what each charge represented, and which ones were genuinely tied to eligible service.

The July 9 My E-rate Guides (MEG) webinar at 11 AM ET is a good place to bring exactly this kind of PIA question. Register today.

About the author: Eric Jester is an E-rate Guide at Funds For Learning. He joined 16 years ago, drawn by a long-held belief in the importance of education and a desire to put his analytical skills to work in communities that benefit from them. Eric leads and develops Guides on one of the Guide Teams, building the processes, alignment, and capacity that let Funds For Learning support clients well. Outside of work, you’ll find him with his wife and daughter (living the cheer dad life), traveling when he can, and playing guitar when time allows.